Policy Update

From Risk to Resilience: How States Are Approaching Insurance and Climate Risk in 2026

March 20, 2026

Overview

Insurance affordability is worsening across the country as insurance companies pull out of entire states and cancel homeowners’ policies due to increased climate risks. States have tried a variety of approaches to tackle this challenge, but a 2025 policy enacted in Colorado (HB25-1182) has emerged as a promising model and inspired a wave of bipartisan legislative action in states across the country this year.

- Why It Matters: As rising climate risks drive insurance providers out of vulnerable markets, states are increasingly advancing policies that seek to transform insurance from a market of uncertainty and rising costs into a transparent tool for community resilience. Several studies have confirmed that investments in climate-resilient infrastructure have proven insurance and economic benefits. To this end, more states are seeking to require insurers to (1) share information with policyholders about how they can decrease their disaster risk and (2) mandate discounts for actions taken to minimize household risk from disasters.

State Spotlight: Colorado

Colorado’s 2025 bill (HB25-1182) has become a model for other states seeking to make insurance markets more transparent and effective for households in the age of climate change. The bill requires insurance companies to (1) be transparent about what models they use to calculate disaster risk, (2) identify for the consumer what actions they could take to reduce that risk, and (3) factor both community and household mitigation measures into pricing and underwriting.

2026 State of Play: Insurance and Disaster Model Disclosure

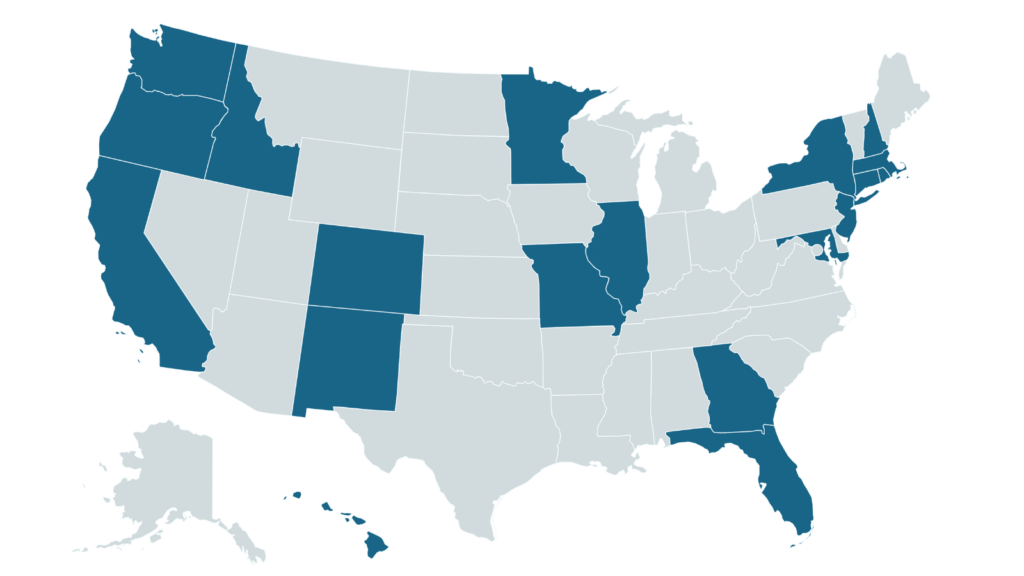

In 2026, at least 18 states have introduced legislation to reform insurance programs to be better prepared for disaster risk and enhance consumer protection.

Of these 18 states, many have introduced legislation in 2026 that build on Colorado’s HB25-1182 to incorporate mitigation measures into disaster risk models: Washington (S.B. 5928/H.B. 2277), Oregon (S.B. 1540), Hawaii (S.B. 2947), New Mexico (H.B. 204), Idaho (H.618), Georgia (S.B.585), and New York (A.9016A/S. 8583). The bills primarily take a two-pronged approach:

- Transparency: Require insurance companies to disclose the factors that go into their disaster risk model and empower the State Insurance Commissioner to challenge models that do not appropriately consider mitigation measures.

- Consumer Empowerment: Provide examples of actions households can take to mitigate the risk to their property, thereby reducing their insurance premiums. Mitigation measures can include fortifying roofs, clearing wildfire defensible space, strengthening structural foundations for earthquakes, and more, depending on the disaster type.

Stay Informed With NCEL

In a time when households across the country are facing rising insurance rates or loss of coverage altogether, states are looking for ways to protect policyholders and to ensure insurance companies are adapting to a rapidly changing environment. Learn more about how states are addressing insurance on NCEL’s Climate Finance Issue page.